The trend is your friend … and so is machine learning

Grasping both general market trends and finer details, a new, hybrid machine learning model from researchers in the Department of Mechanical Engineering predicts financial market volatility with increased accuracy.

With volatility so closely tied to investment risk and returns, it’s no wonder that a statistical method that captured time-varying volatility was deemed worthy of a Nobel Prize. Since its creation, many financial institutions have adopted variants of the autoregressive conditional heteroskedasticity (ARCH) model to forecast time series volatility. Most of these models, however, are not generalizable to all market conditions due to their inability to capture nonlinear market features.

Researchers in the Department of Mechanical Engineering at Carnegie Mellon University have created a new, hybrid deep learning model that combines the strengths of GARCH (Generalized-ARCH) with the flexibility of a long short-term memory deep neural network to capture and forecast market volatility more accurately than either model is capable of on its own.

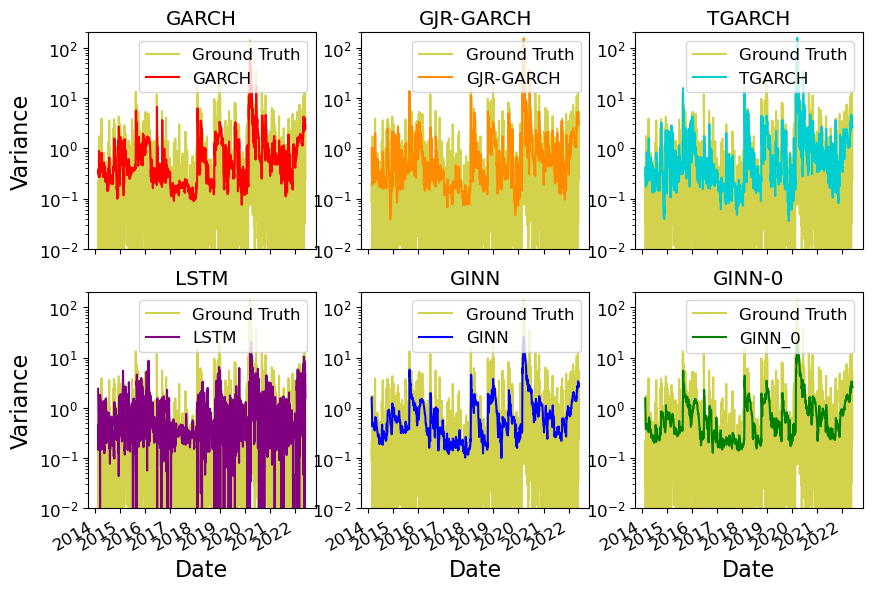

Daily volatility prediction results from all tested models on the out-of-sample testing set on the S&P 500 In

Inspired by physics-informed machine learning, which directly embeds physical laws into the architecture of a deep learning model, the team merged machine learning with stylized facts, which are empirical market patterns captured by the GARCH model. This way, the new model, GARCH-Informed Neural Network (GINN), can learn from both the factual ground truth and the knowledge acquired by the GARCH model to grasp both general market trends and finer details.

Not only will investors who use GARCH as a resource be interested in these results, but our model is valuable for other applications that involve time series modeling and prediction, like autonomous vehicles and GenAI.

Zeda Xu, Ph.D. candidate, Mechanical Engineering

“Traditional machine learning models risk what we call ‘overfitting,’ and is something that happens when a model too closely mimics the data it’s been taught,” explained Zeda Xu, CMU Ph.D. student and lead author of the paper that was presented at the ACM International Conference on AI in Finance. “By building a hybrid model, we ensure generalizability and improved accuracy.”

GINN performed 5% better than the GARCH model alone, and the team saw a noticeable performance increase in predicting the volatility of daily close prices across seven major stock market indexes worldwide against competing models.

“Not only will investors who use GARCH as a resource be interested in these results,” said Xu, “but our model is valuable for other applications that involve time series modeling and prediction, like autonomous vehicles and GenAI.”

“This is a great example of the power that engineering methods can bring to other domains,” said Chris McComb, associate professor of mechanical engineering. “By taking inspiration from physics-informed machine learning, and working closely with subject matter experts, we have introduced a new avenue to construct general time series models for forecasting.”

This research was done in collaboration with John Liechty at Pennsylvania State University, Sebastian Benthall at New York University, and Nicholas Skar-Gislinge at Lund University with funding from The Defense Advanced Research Projects Agency.