Regulators have been giving utilities higher returns. Why?

Electric utility regulators claim to use a model to decide how much a utility should earn. But the data don’t support that idea, as returns to utilities have steadily risen over the past 40 years. CMU researchers try to understand what they might be doing instead.

For many years, all electric utilities in the U.S. were regulated monopolies. Although some states deregulated electricity generation over the past 20 years, electric utility companies in other states today remain monopolies. Providing an essential service without facing competition, unchecked monopolies have little incentive not to overcharge customers. This presents an obvious problem.

To address the issue, public commissions oversee these regulated utilities. Regulators decide how much utilities are allowed to charge in an effort to balance allowing the company to earn a fair return while also protecting consumers.

In their recent paper published in Energy Policy, Paul Fischbeck and David Rode show that this balance between utility companies and their customers has been shifting over time, in favor of the utilities.

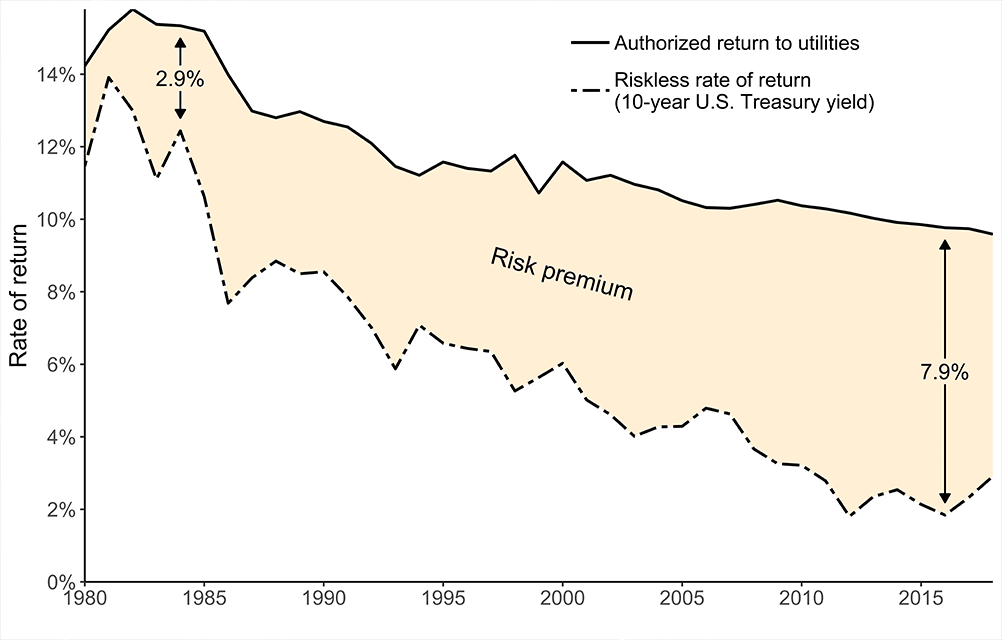

Fischbeck, a professor of engineering and public policy (EPP) and social and decision sciences (SDS), and Rode, adjunct research faculty at the Carnegie Mellon Electricity Industry Center, analyzed almost all of the electric utility rate cases in the U.S. from the past 40 years, a dataset consisting of roughly 1,600 cases. They found a growing gap between the rates authorized and the “riskless rate,” or the rate of return for an investment with zero risk (like U.S. Treasury bonds). This gap is known as the risk premium.

“We noticed that, as interest rates declined over the past decade, the returns regulators were allowing utilities to earn didn’t decline by as much,” said Rode. “This created growing returns for utilities.” The average risk premium in 1980 was about 3%. Today, it is nearly 7%.

Source: College of Engineering

The growing gap: regulators have not kept up with falling interest rates, leading to higher returns for electric utilities.

Regulators are free to set rates by a variety of means. U.S. Supreme Court decisions that established the regulatory framework did not mandate any specific method, only that the result should be fair to both consumers and utility companies.

In many rate cases, regulators claim to rely on the “Capital Asset Pricing Model” (or CAPM) to set their rates. Fischbeck and Rode, however, found that regulators must be doing something else. Relying solely on CAPM would not result in the growing returns that they saw in the data.

“What regulators should do, what regulators say they’re doing, and what regulators actually do may be three very different things,” said Fischbeck.

What regulators should do, what regulators say they’re doing, and what regulators actually do may be three very different things.

Paul Fischbeck, Professor, Engineering and Public Policy and Social and Decision Sciences

So if not basing their decisions solely on CAPM as they report to, what are regulators doing instead?

“We examined potential explanations outside of traditional financial theory,” said Rode, turning instead to behavioral economics. What they found “showed more promise in explaining the data, but also revealed costly biases in the behavior of regulators.”

One such bias is that the average authorized rate of return has leveled off at 10%, even as interest rates have continued to decline. A leveling of rates at the round number of 10% points to a phenomenon repeatedly observed by economists: investor behavior can be influenced by headline numbers, even though the underlying theory is based on the spread between those numbers and the riskless rate of return. Fischbeck and Rode suspect that regulators are hesitant to let the nominal rate of return dip below 10%, despite it resulting in the real rate of return continuing to increase. This sort of bias is known as “money illusion.”

Another factor influencing authorized rates is whether or not a case was settled or fully litigated. Settled cases, where regulators and utilities negotiate a rate, tend to result in significantly higher returns for the utility companies.

Even small deviations from financial theory in the decision-making of regulators can have a huge impact, said Fischbeck. “An error or bias of merely one percentage point in the allowed return would imply tens of billions of dollars in additional cost for ratepayers” and how much utility companies profit.

“Regulators in Canada and in some U.S. states,” said Rode, “use formulas that automatically determine rates as market conditions change.” A mathematical formula would remove the possibility of subtle or unconscious bias in the decision-making. “These authorized rates of return also tend to be lower,” said Rode.

Fischbeck and Rode have uncovered a puzzling trend in the authorized rates from regulators for utilities: the risk premium has gradually increased over the past 40 years, highlighting a disconnect between what regulators claim to be doing and what they are actually doing. The authors hope their study brings attention to the subtle factors that seem to be influencing regulator behavior, and prompts a change to more systematic rate-setting.